4in10 Newsletter 30.11.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 16.11.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 2.11.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 19.10.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 21.9.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 7.9.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 10.8.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 13.7.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 29.6.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

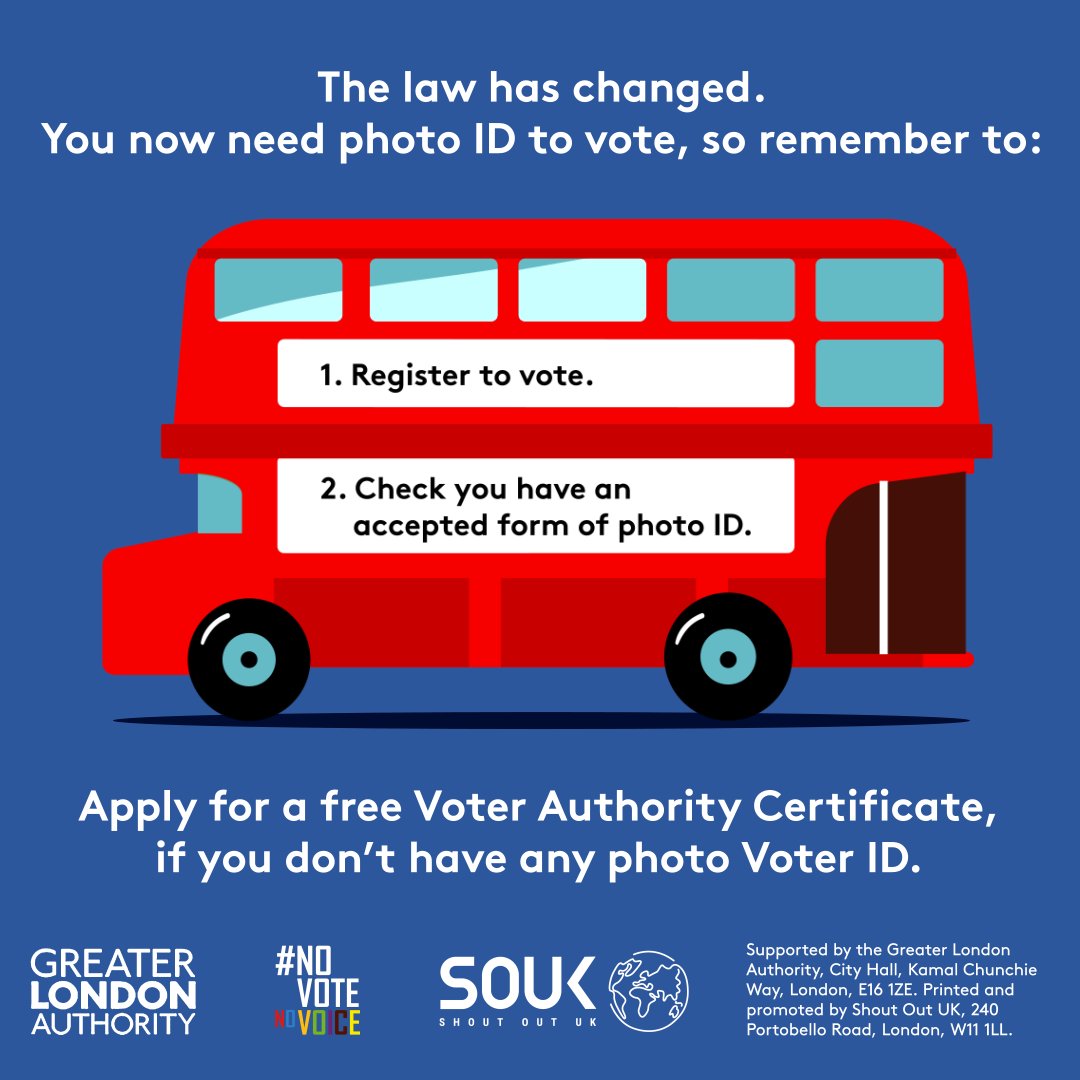

Voter ID and Shout Out UK

A few months ago there was a change in how elections are run in this country, when the Elections Act 2022 came into force

The Act bought in a wide range of changes that will have an impact in London including removing second preference voting in Mayoral contests, but arguably the biggest change was the introduction of compulsory voter ID.

This was trialled in the local elections in May this year to mixed success. The Electoral Commission’s full report is not due out till September but their initial findings have been so troubling that they have released an interim report. This can be found here. The biggest takeaway for me from this was that 14,000 people were not able to vote as a direct result of these changes.

The most significant reason for this does seems to have been lack of awareness of the new rules – only 84% of people knew about the new requirements according to the interim report. I would here quote a family member who when reminded of the need to bring ID said ‘well I never have to in the past’.

Another issue which is of particular concern for us in 4in10 however is unequal access to the right forms of ID. The House of Commons Library produced a report in which they said:

‘The proportion of respondents to the Electoral Commission’s Public Opinion Tracker 2022 who did not have a suitable form of ID for voting was higher among more disadvantaged groups. 14% of unemployed people, 10-17% of those living in rented local authority or housing association accommodation and 7% of people with lower levels of education did not have a suitable form of ID.’

Indeed the interim report found that two of the groups were awareness was lowest was among younger age groups (18 to 24-year-olds) and Black and minority ethnic communities which were both at 82%.

Valid forms of ID

The other issue that continues to be of concern is the types of valid ID. The list of ID that is accepted can be found here.

If you have a look at this list, one thing that becomes immediately clear is that the majority, if not all, of the options available cost money to obtain – a passport for example costs a minimum of £90 once you take into account the cost of the photo.

Some would then counter with the fact that in theory you can obtain a ‘free’ form of ID from your council but even this isn’t completely free as you are expected to bring a passport style photograph with you.

For some families that are already having to choose between heating and eating, paying for a photo to be produced and then spending time finding and filling in a complicated form simply can’t be a priority.

This can be shown in that awareness and take-up of the Voter Authority Certificate (a free voter ID document you can apply for) was low with only 89,500 certificates being issued around the whole Country according to the Electoral Commission’s interim report.

The London Context

London already has one of the lowest voter registration rates in the UK and these changes has the potential to make this situation considerably worse.

There are many reasons for this but one of the biggest is the high proportion of ethnic minority communities in London. Voter registration tends to be lower in ethnic minority communities. This is the case for many reasons, including in particular insecure, short term housing but no matter what the cause the result remains the same.

We at 4in10 are concerned that unless more is done to raise awareness of the new rules and to make it easier and cheaper to obtain the necessary ID, then Londoners who are already at most at risk of being disenfranchised will be denied the right to vote.

That is why over the last few months we have been supporting Shout Out UK who have been leading the public awareness campaign on this issue and we will continue to do so.

We are asking our membership to help us and Shout Out UK by spreading the word about it and where possible help people to get the ID that they need. Find out how here.

4in10 Newsletter 15.6.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

Child Poverty in London: a societal problem calls for community-led solutions (Part 3)

Our Research and Learning Officer, Emily, discusses three questions on the issue of child poverty in London. This piece is split across three blog posts:

- What is child poverty?

- What’s the state of child poverty in London?

- How do we end child poverty?

How do we end child poverty?

This is a big task. Let’s say tomorrow the government printed money and gave it to every family under the relative poverty line and promised to keep sending them money to ensure they never fall below that line, would child poverty end? If that question were posed to different politicians and members of the public, I’m sure several revealing answers would emerge. The reality is that things are much more complicated than just money. But as a start, money really does help. The £20 per week uplift to Universal Credit that was temporarily put in place during the pandemic pulled 400,000 children out of poverty. Other estimates claim that making this permanent would lift 500,000 children out of poverty. So money must be part of our child poverty strategy. So too would other public systems. Having an adequately sustained NHS and mental health services would keep children and their parents well, which cuts costs, both in terms of health itself and the knock-on effects of poor health.

Flexible working could also be seen as a support structure to allow adults, particularly women, to work consistently and progress in their careers while also caring for their children. And there’s also the housing issue. In London housing is incredibly expensive and too many affordable options are unsuitable. Guaranteeing affordable homes for everyone can be seen as part of a child poverty strategy.

So it’s about money, but it’s also about a community-based strategy. We need to eradicate the shame. There is no reason to judge people. Ending shame is not ending personal responsibility. Ending child poverty requires us to work together. It means believing the evidence that shows the causes of inequality and poverty are multiple and intersecting. It also means, perhaps, as a community taking on the shame that we don’t yet know how to support each other well enough. Privilege and discrimination has blinded many of us to our own personal responsibility. We can do better at that, but we need to be honest about our role and how we can learn to support each other more holistically and with respect.

4in10, London’s Child Poverty Network is committed to supporting collaborative working. We are a network of organisations who want to see an end to child poverty in London. There is so much brilliance bottled up in the children of this city. When we invest in them and make sure each of them has an opportunity to thrive, then we will begin to see transformations that we will all benefit from.

London’s Child Poverty Alliance, the policy sub-group of London’s Child Poverty Network has identified four key areas that can be catalysts for change. In our Manifesto, we outline current areas of inequality and systemic failure that are points of potential transformation that could ultimately bring an end to child poverty in London. Secure, adequate income will give families the resource to access what they need. All across London, our homes are fundamental to our health and wellbeing. When our homes are of decent quality, the comfort and security they provide enrich our lives and support our mental and physical health. Every child deserves the best start in life, ending child poverty means ensuring every child has access to the early education and childcare to thrive. Lastly, having access to nutritious and reliable food sources so that all children are free from hunger can target one of the essential threats of child poverty. Together, we can make child poverty a way things used to be rather than how we live now if we target these four areas as crucial pinch points of poverty to make London a fairer city for every child.

Child Poverty in London: a societal problem calls for community-led solutions (Part 2)

Our Research and Learning Officer, Emily, discusses three questions on the issue of child poverty in London. This piece is split across three blog posts:

- What is child poverty?

- What’s the state of child poverty in London?

- How do we end child poverty?

What’s the state of child poverty in London?

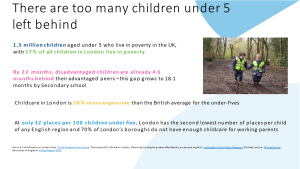

Unfortunately, the number of children in poverty across London is extremely high. The latest figures from 2021/22 show that London has a child poverty rate of 32.9% according to End Child Poverty Coalition. We expect this to increase when the current year’s figures are released. Experiencing poverty can mean children are only able to afford cheap, unhealthy food. It might mean they skip washing their clothes, bathing and brushing their teeth. It can result in anxiety and isolation, aggressive or regressive behaviour. Being trapped in poverty can lead to a stressful environment at home, where children feel like they need to take on adult responsibilities to help out. While all these things can be true for any child of any household income, the likelihood of overlapping challenges or examples of ‘going without’ can be much greater when a child is in poverty. Parents can be doing the best they can with what they’ve got, but they can’t absorb all of the trauma that impacts them and their families.

How do we respond to child poverty?

The government prioritises helping families get into work. This can be one valuable, effective way to help families in poverty. However, it’s important that context is considered. For one, balancing children’s needs with a work schedule is very difficult. So, for single-parent families flexible, adequate work is crucial. In addition, some parents can’t work because either they or their child is disabled and therefore more support is needed that looks different than paid work. Also, illness needs to be considered as some adults can’t work because they are dealing with an acute illness. Therefore, as a society, we have to think about helping families get support and money in their pockets and community connections that look beyond the paid work route out of poverty.

At 4in10, we talk about supporting organisations who work to end poverty or mitigate its impact. To end child poverty would be to ensure that families have the income they need to cover the essentials. This can look like a robust social security which puts money back into the pockets of families, it can also look like higher pay which increases the incoming funds on a regular basis and it can also take the form of organisational tax breaks or social investment in services so that more support is freely available which reduces the need to ‘buy in’ to participate in local communal activities and opportunities.

In terms of mitigation of the effects of child poverty, again, some specific considerations help draw out this point. Children know when they don’t have as much as others. Children are experts in observation, they learn from seeing and doing and so they know when things are different. When it comes to household finances, they may not know the details or understand the specific issues, but children are capable of knowing when they have less or shouldn’t ask for more. As part of communities all across London, we can help nurture belonging and fairness by making it easy to share resources, reduce additional expenses at school and offer out-of–school activities that are free of charge and sustainably developed and delivered. By making it less about what you can buy and more about where we can belong, the organisations such as youth clubs, art groups, theatres, community organisations, schools and many other community-led programmes help children access support and meaningful relationships with those local to them. This can create a buffer between children and the impact of poverty on their wellbeing. These kinds of services will always be important, even if child poverty disappeared from London. Their existence helps offer important outreach to children and their families. It’s important that these organisations can focus on what they do best, but the current system demands them to follow the money in terms of endless cycles of grant submissions, reporting and project adaptation to keep the budgets balanced. This makes losers out of all of us. Funding can and should be sustainable.

There are steps that all of us can take in our organisations and as individuals to help advocate and implement change. In our Manifesto for a child poverty free London, we outline four key areas that would help reduce child poverty across London. Income, housing, childcare and hunger. These four areas impact us all and in different ways, individuals, businesses, local, regional and national government can help contribute to make the situation better for children. This is not about attributing blame on any one group, but about community-centred and multi-faceted responses to helping improve the lives of children and challenging inequalities when and where we see them.

Child Poverty in London: a societal problem calls for community-led solutions (Part 1)

Our Research and Learning Officer, Emily, discusses three questions on the issue of child poverty in London. This piece is split across three blog posts:

- What is child poverty?

- What’s the state of child poverty in London?

- How do we end child poverty?

What is child poverty?

The very fact that children experience poverty across London reflects the failings of British society to support its youngest members. Children are experiencing poverty because their guardians don’t have enough resource to meet their basic needs. Despite their care givers’ best efforts to protect them, children in poverty can experience the stress and insecurity that stems from not having enough to meet essential needs and some children even take on the practical or emotional responsibility to help alleviate some of the worries of the adults in their household. Children don’t choose poverty. And they can’t choose to end it. They rely on adults in their community, both local and national to make the changes necessary to ensure they, as children, get what they need.

Relative poverty is defined as a household income that is 60% below the median income. While children are in poverty across the country, they may not experience it in the same way. In London, housing costs and childcare costs mean that children in London are more likely to live in unsuitable accommodation and fewer access early years education whereas in other parts of the country, the challenges may be high travel costs or their adult carers experiencing difficulty finding work.

What causes it?

The simple reason for what causes poverty is that household income isn’t enough and is far below the average of many other households. The much more complicated answer is that inadequate income can be the result of an inability to work, poor health, disability, discrimination or unexpected change of circumstances or a combination of challenges that lead to income insecurity. Where it gets really complicated is that accessing adequate income is not a case of simply trying to secure more work because often suitable, paid work is not accessible, for example because of prohibitive childcare costs. This is where narratives around personal responsibility and shame can take root and spring life to inaccurate descriptions as to why some people have enough and others don’t.

Child poverty is caused by both indirect and direct policy decisions related to children. For example, financial budget reductions for schools, youth services and community organisations mean that children are cut off from the services meant to serve them specifically and in turn it’s only those who can afford to pay for those same services that get the high quality opportunities that help shape children’s present experiences to lead to privileged future opportunities. In addition, policies that impact wages, housing and service provision across the country mean that adults can’t access the jobs and support they need, which has a knock-on effect for children. In combination, these circumstances exacerbate inequality making a greater divide between those who can afford to pay extra and those who can’t afford the essentials.

What makes child poverty different?

One of the worst parts of child poverty is that it hurts people at a crucial time in their lives when poverty is integrated into their physiological systems. When their bodies and minds are developing rapidly, and their emotional regulation is dynamically maturing, the trauma that poverty inflicts has a lasting impact. While adults might feel the burden of responsibility, they also have more political influence as voters. Children do not. They can’t work, they can’t vote and they can’t always access the people with power and influence to change. So, they are made to wait and struggle.

4in10 Newsletter 1.6.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 17.5.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

Spotlight on 4in10 Member Whizz-kids

How are you helping to tackle child poverty in London?

We work to support young wheelchair users through 3 main strategies – Mobile, Enabled, Included. All of which have an impact upon the potential for poverty faced by young Londoners with a disability.

We enable young people to have a chance to have a childhood through our free clubs and programmes, aimed to break the isolation of disability, and give the young people confidence, social skills and a group of friends. At no cost to the family, these can help to tackle the mental impacts of financial deprivation. For young people who are older, we also supply free Employability skill and work placement with our network of partners to provide the launchpad for young wheelchair users to beat the employment gap, and to aid in systemic change to a less impoverished disabled generation.

Tell us something you are excited about?

Morph! Yes, Morph! This year across the summer, Whizz-Kidz has teamed up with Wild in Art and Aardman Animations to do the first step-free Art Trail within London. The trail will have 50+ 6ft high Morph sculptures painted and designed running down the Southbank from Tower Bridge then across past St Pauls and into the city. Alongside the “big” Morphs will be “gaggles” of ‘Mini’ Morphs, designed and painted by schools to support the trail, and of course to support Whizz-Kidz.

Pop along between June and August to see Morph having an “Epic Adventure” in London!

Share with our members something positive about your organisation’s achievement or service?

It has been shown repeatedly that the right wheelchair can a big impact on a young person, both mentally and physically, allowing them to access education, recreation and employment with a greater ease and confidence. Through the Mobile strategy, Whizz-Kidz supported approx. 1,000 families through our clinical services, of which near 1/3 were from the most deprived parts of England, helping to alleviate disability related costs averaging £2,400 per piece of equipment, whilst giving a young person the same chances and childhood of non-disabled children.

What can other network members learn from you or find out more about through you?

Our work to make our young people more included starts and ends at their voice, aims and ambitions. The Kidz Board, a group of 12 young people that help to guide and steer the organisation onto topics that are concerning to them as young disabled people, has allowed us to look at the issues around poverty and financial deficit of the disabled community from all the angles impacting their daily lives. Examples have included the non-standardised “disabled bus pass”, longer journey times due to inadequate higher education accommodations, the job market, social activities, the role of assistance dogs and many more – all of which have a financial impact on young person and their family.

What would most help you achieve your goals?

Whilst of course, funding is always helpful to a charity, we are always looking to be raising awareness of the additional issues faced by Young Wheelchair Users, as quite often they go unnoticed. Partners committing to having Disability Awareness provided by people with lived experience, or work with people with lived experience to open their horizons, and break the misconceptions around disability. The young people that we work with also need people to provide them with the opportunities to succeed, whether that is in a social setting through supporting our clubs, or a employability setting supporting Work Placements and Employability Skills Sessions.

Show these young people that they have a future just like anyone else.

Why did you join 4in10? What do you enjoy about being part of the 4in10 network?

We joined 4in10 as we have become rapidly aware of the additional effects of having a disability on the Cost of Living, and Child Poverty issues currently within the UK, and London. As an organisation that helps to support these young people, we know that we need to be connected to others fighting this issue as well. A candle is dim, but a handful can become a lighthouse, after all.

It is great to be part of a group of organisations looking to tackle this issue within London, a city often shown by its tourist-y bits and not some of the areas of great deprivation and be able to talk about the work we are doing, and ask to help from others on the topic, and campaigns we are running.

To connect with other groups who are interested in childcare and child poverty. So far its been really useful, thank you!

4in10 Member Conducts Research on Low-Income Families and SEND Support

Over the past several months, 4in10 has been working with one of our members, Education and Skills Development Group (ESDEG) to support them in creating an excellent report that outlines the importance of their work with low-income ethnic minority families with children who are eligible for SEND support. With a financial contribution from 4in10, Suchismita Majumdar, ESDEG’s Communications & Policy Officer conducted comprehensive interviews and analysis with the ESDEG team to get a sense of the particular needs and challenges children who require SEND support face when they and their parents seek access to additional support.

The report takes an impressive introspective look at the programmes ESDEG offers and the support they give to children and their parents in response to the particular needs of specific ethnic groups, in particular, Somali, Pakistani, Afghan, Indian and Black Caribbean communities.

Their report, available here, shines a light on the situation both for non-white families across London who encounter barriers because of cultural and economic stigma as well as the more widespread scarcity of SEND programmes and professionals in the state school system across London.

The report also includes some key evaluations that ESDEG has identified to help guide them as they plan and implement future programmes, policies and campaigns going forward.

4in10 Newsletter 4.5.23

Read the latest ewsletter here.

To get this directly to your inbox every fortnight please do join us.

How Poverty Feels

In 2021, 4in10 in partnership with the Greater London Authority commissioned ClearView Research to speak with Londoners to understand what poverty felt like since the Covid-19 pandemic had hit. What Londoners said helps paint a picture of the challenges that so many people face.

All of us across the city have ambitions and there is plenty of opportunity to go around, but it’s been ring-fenced for a small group of people leaving many with too little left. The report showed that with an inadequate social security system, many families found the challenge of gaining secure employment, suitable housing, affordable childcare and everyday costs out of reach. Despite having big dreams, many felt that they were fighting forces beyond their control, an experience compared to flying against gravity.

In 2023, with numerous strikes occurring on a regular basis, it’s clear that workers in many sectors feel they are at breaking point highlighting that the foundations are in need of repair. Basic transportation, health and teaching services are woefully underfunded and lacking investment for innovation and expansion. It’s worth revisiting this report to understand what families are facing today.

Families can’t strike, they have to keep up the fight despite recent data showing that low-income Londoners have faced 21% inflation over the last three years. Families are choosing between heating and eating and the prospect of focusing on career progression when your flat is mouldy and transportation is unaffordable and childcare is inaccessible is an impossible challenge.

What Londoners asked for in the report was for government to make the basics affordable. If childcare, cost of living bills and transportation were affordable then the possibility of families accessing better employment and housing that would enable them to thrive could come to fruition. This is what a good social security system does, it ensures we all have what we need through a social investment for us all. We need policies shaped by all of us to ensure no one gets shut out of decisions that affect them.

Revisiting this report from 2021 is worthwhile because its key findings still hold their weight. That is that poverty is something most of us are concerned about and 85% of us believe that politicians should do more about it.

With local elections just around the corner and London mayoral elections and a General Election on the horizon, it’s worthwhile thinking about making sure politicians hear from you that ending poverty warrants strategic policies. It must be a priority if communities are to thrive, and industries continue to expand providing income sources for Londoners. Flying Against Gravity shows the experiences of Londoners in first-hand accounts that remind us of the emotional toll that is unacceptable.

Together we can do more by demanding lasting change to ensure we all have what we need to soar.

4in10 Newsletter 20.4.23

Read the latest ewsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 6.4.23

Read the latest ewsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 23.3.23

Read the latest ewsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 23.2.23

Read the latest ewsletter here.

To get this directly to your inbox every fortnight please do join us.

Spotlight on 4in10 Member On The Record

![]()

How are you helping to tackle child poverty in London?

The lack of affordable childcare and inequality in educational opportunities for the early years is a major cause of poverty. Our project ‘Grow Your Own’ is sharing the history of how people created childcare and early years education and campaigned for improvements in London from the 1960s till the present day. We hope that learning more about how childcare was created in the past could help people change the childcare system we have today for the better, and therefore help to tackle child poverty.

Tell us something you are excited about?

We are excited that we can offer 10 free places on a podcast training course running from April 20th for six weeks. People taking part will get expert training in writing, recording, researching and editing a podcast episode, with all expenses covered including childcare. If you are affected by the lack of affordable childcare or trying to change childcare for the better, and have a connection to east London, please apply to join the course!

Share with our members something positive about your organisation’s achievement or service?

We’ve only just begun, but we have found a lot of people already with really interesting stories to share from decades of work making childcare better. We are starting to plan a program of events where we’ll share some of that experience and learning.

What can other network members learn from you or find out more about through you?

About the history of childcare, including how parents set up their own community run nurseries in the 1970s when they couldn’t find any childcare, how they campaigned to get their local councils to fund them, and how their work setting up community nurseries directly influenced the Sure Start Children’s Centres that were set up in the late 1990s. We want to get the most useful information to you to help you achieve your goals today.

What would most help you achieve your goals?

Reaching lots of people – so please help spread the word!

Why did you join 4in10? What do you enjoy about being part of the 4in10 network?

To connect with other groups who are interested in childcare and child poverty. So far its been really useful, thank you!

4in10 Newsletter 8.3.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

Children with special educational needs and disabled children

4in10 organised a coffee morning in February 2023 that was jointly hosted by staff and parents at Marjory Kinnon School in Hounslow. Rochelle McIntyre, the Family Support and Community Outreach Worker facilitated the discussion and had invited her colleague Jo Stacey, Assistant Head Teacher, Key Stage 2 and Staff Governor as well as a parent to provide first-hand experience.

This mother shared her experiences as a single-parent and the challenges of caring for a child with autism. Throughout the group discussion, a few key costs were mentioned that demonstrate the challenge of parenting and educating children with a learning disability. These include:

- Changing dietary needs and specific food items being essential to meet the sensory needs of the child, these foods are often more expensive or difficult to predict and buy reduced

- Clothing and textures becoming uncomfortable leading to new purchases frequently

- High costs to attend a sensory appropriate gym, averaging £17.50 per visit which swallows up a high proportion of the Disability Living Allowance (DLA) that her son is entitled to

- Taxis across London for appointments as the underground is too overstimulating

- This parent shared that her son often strips off his clothes at home meaning its particularly important to keep the house warm enough, thus adding to the cost of utilities.

The emotional side for parents was also highlighted. A parent in attendance explained that working part time and taking coursework all had to stop because it just became too overwhelming for her and exhausting to keep up. Even when she was able to access a personal assistant, there were still costs associated with the PA taking care of her son or taking him out and about that limited how much her son could do with her PA. Thus, it felt like there were always limitations and challenges as to how much help she could get because the costs keep adding up.

Another parent of a child with autism shared her own experiences and emphasised that practical help is important, but the challenge of supporting and adjusting to the sensory needs of a growing child with autism is always there.

At 4in10, we want to listen to these experiences and share them with those who make decisions that impact children and their parents. We want to highlight the financial and emotional challenges that parents face and the impossible situations that parents with low-incomes encounter when caring for a child with a special need or disability. If you have other thoughts or experiences that you’d like to share, please do get in touch so we can support growing more awareness and social action to advocate for better support of children with varying needs and financial situations.

4in10 Newsletter 9.2.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 26.1.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 12.1.23

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 15.12.22

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

Newham Nurture roundtable

4in10 Manager Katherine reflects on the Newham Nurture roundtable event she attended this week

Earlier this week I had the great pleasure of attending an event that showcased and celebrated the work of the Newham Nurture project. Newham Nurture is a community partnership with NCT, Alternatives Trust, The Magpie Project and Compost London. The programme supports women through pregnancy and up to two years after birth from low income, migrant and marginalised backgrounds experiencing financial hardship and disadvantage. It does this by providing drop-in pregnancy sessions, Baby & Me sessions for mums with babies from newborn up to 2 years, peer support and counselling.

A few reflections…

The project shone out as an example of what good partnership working and co-production ought to be, but all too often isn’t. The women from the project steering group, many of whom also deliver its work as volunteers and staff members, spoke eloquently and movingly about their own experiences of struggling to access the support they needed as pregnant and new mothers, about how the partner organisations were a lifeline for them and how passionate they are about making sure that help is now available to other women who so desperately need it. It was also clear from the discussion that there was a high level of mutual respect between the project partners and local statutory services, with a clear acknowledgement that unless services really listen to and act on what women are telling them then they will remain inaccessible to many.

There is a lot for others to learn from the experience of the project. While Newham’s challenges may be distinctive, there is no doubt that in many other areas of London there are families who would benefit enormously from the support of a project like Newham Nurture. The experience of having a baby can be a daunting and isolating experience for any woman, and if you add to that experience of loss and trauma, very low income, insecure housing, language barriers and discrimination, then this is magnified many times. The event concluded with a powerful audio recording of women who come to Newham Nurture talking about it and what it meant to them. The message that came over loud and clear was that they valued the project not only for the accessible, practical advice and support it gave them but also a place where they and their children could come, feel welcomed and enjoy the friendship of others who have trod similar paths ahead of them. Compost London are evaluating the work and I look forward to reading and sharing their findings with all the other organisations in the 4in10 network so that they can learn from the excellent work that Newham Nurture has planted, grown and is now blossoming in their community.

While the overwhelming feeling I had on leaving the event was one of hope; gained from witnessing the deep commitment that the women who lead this programme have to supporting one and another and working tirelessly to improve the lives of their young children, it was also tinged with anger. Anger that the choices of our politicians are wreaking such damage on these families’ lives and withholding the resources needed to ensure their children’s rights to food, health and education. With no end to the cost-of-living crisis in sight and further cuts to services on the cards, it is alarming to think that the situation for these families will get worse. Drawing on the hope and belief that change is possible, as the project so clearly demonstrates, we must redouble our effort to challenge these systemic injustices and demand better for children and families.

4in10 Newsletter 1.12.22

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 17.11.22

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

Spotlight on 4in10 Member Education and Skills Development Group

![]()

How are you helping to tackle child poverty in London?

At the Education and Skills Development Group (ESDEG) we strive to alleviate child poverty through education in the London borough of Ealing. We run several programmes that provide support to the children belonging to refugee and deprived communities so that they can perform at par with the rest of their school cohort and enjoy a dignified childhood.

Supplementary Schooling: ESDEG was started to help children from refugee and deprived backgrounds to perform better in school. Around 2005 a bunch of us noticed that the attainment rate for children from refugee families in the Ealing was pretty dismal. Somali children were struggling in school and consistently underachieving, so we started after-school homework clubs. Our tutors not only provide children help with academic subjects in particular English, Mathematics and Science, but also offer a safe space to share their experiences in and about school.

Summer Camps: Over summer and other holidays we team up with other local organisations to organise camps, family fun days, seaside trips, sports and other recreational activities because we realise that some of the parents from deprived backgrounds cannot afford to take their children on holidays and day outs.

Family and Schools Partnership: Our work with children and parents made us realise how much some parents from deprived backgrounds whose first language is not English struggle to communicate with the teachers and school staff. The challenge gets multiplied for parents who were not raised in the British education system. From this stemmed our next service, our Family Support Liaison Officers work as a communication bridge between schools and children and their parents. One of the major issues our liaison officers are working on are school exclusions, both formal and informal. We have also produced a research document based on case studies of exclusion cases among the Somali community in Ealing (report available in our website www.esdeg.org.uk)

Youth Mentoring Project: This project is designed to provide individual and group mentoring to inspire young people; help raise their self-esteem and aspirations; improve their attainment and behaviour; and reduce the likelihood of exclusions, crime and anti-social behaviour. We motivate them to study and succeed in life by looking up to successful role models. Moreover, we equip our mentees with the resilience, emotional intelligence and growth mindset to help them overcome their barriers. Our experienced mentors provide structured and engaging sessions to young people from minority backgrounds, offering guidance, support and encouragement aimed at developing the competence and character of their mentees. Young people often disclose concerns and problems that parents/carers and school staff are not aware of. Our mentors also detect and report any safeguarding concerns and help young people overcome issues of abuse, bullying, radicalisation, neglect etc.

Special Educational Needs and Disability (SEND) Project supports children in Ealing with special educational needs and disabilities (SEND). Our aim is to bridge the gap between families, schools and the Local Authority by working with both the parents and the children to ensure the child is receiving all the support they need for educational success. Our specialised staff focus on identifying the reasonable adjustments a child with SEND may need to reduce the disadvantages they face as well as providing extra encouragement in their learning and support with physical and personal care difficulties.

Tell us something you are excited about?

ESDEG’s integrative therapist has recently launched an initiative which encourages school children to express themselves through art. These exercises have been very effective with children who suffer from anxiety. Children not only express themselves more candidly through colours and pencils, they enjoy the process and are eager to come back for more. Seeing the success of this initiative, our counsellor is planning to expand this to other children as well.

Share with our members something positive about your organisation’s achievement or service?

Last year (2020-2021) we supported over 180 students through our supplementary schooling – helping to raise their academic achievement, self-esteem, and social skills. Over the last seventeen years since ESDEG started, we have seen the children who attended supplementary schools improve their performance in school, secure college places and go on to have successful careers.

What can other network members learn from you or find out more about through you?

ESDEG works with refugee and minority communities, the so-called hard-to-reach target groups. One of the main reasons for our successful outreach is that many of our staff are from minority backgrounds ourselves. Not only do we belong to the same community and speak the same languages, we understand the cultural and religious nuances which enhance communication and our clients feel confidence in our ability to provide them with high quality services.

What would most help you achieve your goals?

Like the other grassroots organisations we are also striving to operate with a limited pot of funding. Added to that is our struggle to secure office and training/meeting spaces for our day to day activities in the Ealing borough of London. The third challenge we face is in recruitment, training and retaining our staff. We feel that we could concentrate on our work a lot better if these administrative issues could be sorted.

Why did you join 4in10? What do you enjoy about being part of the 4in10 network?

To connect with like minded organisations who are working with disadvantaged groups. Also being part of the 4in10 network helps us be part of the collective voice of the sector.

4in10 Newsletter 3.11.22

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 13.10.22

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 15.09.22

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 1.09.22

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 3.08.22

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 21.07.22

Read the latest newsletter here.

To get this directly to your inbox every fortnight please do join us.

4in10 Newsletter 12.05.22

Read the latest 4in10 Newsletter here.

To get this directly to your inbox every fortnight please do join us.

Read the 4in10 Newsletter 31.03.2022

Action needed, news, information, funding, jobs and more. Get it delivered direct to your inbox fortnightly. Sign up here.

London Elections 2022. Influence your candidates NOW!

London Elections 2022.

Influence your candidates to take action on child poverty.

On 5 May 2022 in all 32 London boroughs apart from The City of London, every council seat is up for election.

This presents a once-in-four-year opportunity to grab the attention of those who would represent us, tell them about the impact of poverty on the city’s children and what they must do to tackle it. With child poverty rates in London among the highest in the country and many families are now facing severe hardship in the face of the cost-of-living crisis, it is a matter of urgency that those seeking election to their local council prioritise tackling child poverty in their communities.

4in10, alongside other organisations in the London Child Poverty Alliance, is asking its members to engage with candidates in these elections to encourage them to sign our pledge to work towards a child poverty free London.

We hope that as a result, on 5 May there will be hundreds of local government elected officials who are better informed about how they can tackle child poverty in the local communities and are ready to take action to do so.

Manifesto for a child poverty free London

The London Child Poverty Alliance’s Manifesto for a Child Poverty Free London sets out twelve key ‘asks’ that it believes if put into action, would make a significant contribution towards creating a child poverty free London. The asks are focused on four key areas:

- Action on income

- Action on housing

- Action on childcare

- Action on hunger

The manifesto website provides prospective councillors with good practice examples, local data and further information about how these can be put into practice in their communities. It also contains a signup page where they can publicly commit to work towards a child poverty free London.

Take part in the campaign

First and foremost, we are asking you to share the manifesto with your staff, volunteers and those you work with and ask them to ask candidates they meet to sign up to the pledge via the manifesto website.

If you have the capacity, you could also send manifesto to the candidates in your ward, or across the area where you are based, asking them to sign the pledge.

The easiest way to find out who your local candidates are is to visit the Who Can I Vote For? website and enter your postcode. Alternatively, you could contact the local offices of the main political parties to ask them for their contact details.

Also look out for local hustings events going on in your community and if possible attend one. These will provide an opportunity for you to ask the candidates what they plan to do to tackle child poverty, you can use the manifesto to help you decide what to ask.

If you need any support or have any questions, please contact us and we’ll be very happy to assist.

Register to vote

And finally, don’t forget to register to vote! It is possible to register to vote even without a permanent address. The deadline to apply is 14th April and the deadline for applying for a postal vote is 19th April. Contact your council’s electoral services team for more information.

Useful resources

London Councils Guide to How elections work

Guidance from the Charity Commission on campaigning during election periods

Interesting Blog from New Philanthropy Capital

What Will Spring Statement the Spring Statement Mean for Charities.

Thank you to NPC for allowing us to share this. For more information click here:

Spring is upon us. Flowers are blooming, birds are finally singing—and the sound of tweeting will reach deafening levels this week as the change of seasons also brings a new Spring Statement from the Chancellor. But as new beginnings go, the outlook has looked brighter.

A lot has happened since the somewhat optimistic-feeling autumn budget, and not much of it has been good for the charity sector: a war in Europe, the subsequent economic and social fallout, and spiralling living costs across the country. With this backdrop, ‘levelling up’ has dropped down the agenda, but it cannot be forgotten. More than ever, we need to see the budget deliver for marginalised groups who are most vulnerable to these social and economic shocks.

What will be the big themes of the budget?

In the short term, the overall economic outlook is pretty bleak. Inflation is rising to 30-year highs and may hit double digits, with another spike likely in the autumn. Disposable income is set to see the largest annual fall in 50 years. The government already announced a rise in the National Insurance rate—and although they may be scrapping this for the lowest paid workers, it will provide little salvation to those most affected by rising costs. The Chancellor has teased that rising food and fuel prices are likely to be confronted with a package of support, in addition to the £350 package announced in February—which now seems like a drop in the ocean. However, rumoured defence spending rises and support for Ukraine may limit the Treasury’s ability to ease people’s concerns.

We also have huge labour market vacancies, with around 1.2 million fewer people in the labour market compared to pre-pandemic trends. This is driven both by the young, but also by over 50s who have left the labour market completely. The Treasury will likely be thinking closely about this and an update to the plan for jobs is expected on Wednesday.

What should charities be expecting?

There may be tough times ahead for the charity sector. The combination of rising costs, rising demand and inflation, leading to a decline in value of grants and donations, could be a serious one for charities. What is certain is that as an abstract ‘cost of living crisis’ moves into a desperate ‘can’t heat my home’ crisis, charities will be ever more in need.

Along with the support for household bills already mentioned, there have been some rumoured benefit changes which the Chancellor may employ to try and soften the blow. For example, lowering the taper rate of Universal Credit again, or raising child benefit or pensions, but in the short term this is unlikely to seriously alter the circumstances of many people that charities support.

Charities whose work concerns Ukraine should also expect specific announcements around the crisis—both in terms of more support for resettling people in communities here, and also in terms of increased aid for organisations working closer to Kyiv.

What about levelling up?

With everything else that’s in the news, the mission to ‘level up’ the country has fallen down the agenda. However, the pain people will be feeling over the coming months means that this support is needed more than ever.

The largest levelling up fund yet to be allocated is the UK Shared Prosperity Fund (UKSPF). This is meant to replace EU funding for business support, community infrastructure, and employment and social exclusion support. The prospectus for the UKSPF is due soon, and allocations to lead authorities may be made as early as the Spring Statement. Given the labour market vacancies, this would be welcome.

What may be missing, however, is support for tackling social needs. In the pre-launch guidance for the UKSPF, the government quietly revealed that new funding for people and skills may not be available until 2024 / 25. As we outlined in our recent briefing, this could leave a three-year gap in new funding which will affect the most marginalised in the country the most, and will risk progress on the levelling up agenda.

At NPC, we’re worried this is going to blunt charities’ ability to deliver for communities around the country at a time when they are needed most. Following on from our briefing, we will be running an event on the UK Shared Prosperity Fund next month, focused on how charities and local government need to work together to ensure people don’t lose out on support. This will be vital viewing for anyone trying to tackle social exclusion or improve employment in communities around the country. Further details announced soon.

Longer-term, we are focused on ensuring that the lessons from projects working on social issues around the country are kept at the heart of future levelling up plans. Later this year, the government will be launching its Strategy for Community Spaces and Relationships. We know how much there is to learn from work that’s already happened, and we will be pulling together best practice from community initiatives across the country, along with fresh thinking, to design plans that can genuinely tackle the social needs that people see as key to the success of levelling up.

The Spring Statement is unlikely to bring a new start for the charity sector, but we know many charities have already planted seeds which address the issues communities care about. We want to help them grow and thrive elsewhere.

Get in touch with Theo.Clay@thinkNPC.org if you want to learn more.

Read 4in10's Latest Newsletter Here

News, Campaigns, Data, Funding and More.

To receive our newsletter every fortnight directly to your inbox, join us here.

Spotlight on 4in10 Member Praxis and the NRPF Action Group

How are you helping to tackle child poverty in London?

Praxis is a charity for migrants and refugees. We provide immigration advice, housing and peer support and through all of these ways our work helps to protect children from poverty. We have become a leading expert in finding pathways out of destitution and supporting migrants facing homelessness, and our training and campaign work has national and international impact. Our core purpose is to help migrants in crisis or at risk, ensuring they can live in safety, overcome the barriers they face, and take control of their own destinies. You can read more about our strategy here, find us on Facebook, Twitter and our website here.

As part of this work, we facilitate the No Recourse to Public Funds Action Group, which is made up of campaigners with lived experience of the No Recourse to Public Funds (NRPF) policy, to build campaigns to end this policy. You can find out more about our campaign, and read the NRPF Action Group’s manifesto calling for the end of NRPF here.

Tell us something you are excited about?

We are really excited that the group has decided to focus on campaigning for free school meals. The overarching goal of our campaign is to ensure free school meals for all children living in poverty, regardless of their parents’ immigration status. We’re launching with a specific call to the Government to make permanent the temporary extension of free school meals to some groups of children living in poverty affected by No Recourse to Public Funds, which was brought in during the pandemic.

We are also calling for free school meals for all children in poverty, regardless of immigration status, to take into account the fact that children with insecure immigration status are not covered by the extension of eligibility.

Our policy briefing sets out our campaign asks in more detail – you can find that here;

Additionally, here are some posts you can share if possible:

- Facebook: https://www.facebook.com/PraxisCommunityProjects/posts/325409016299148

- Twitter: https://twitter.com/Praxis_Projects/status/1500765019050500096

- Instagram: https://www.instagram.com/p/CazDWYtoCQa/

- LinkedIn: https://www.linkedin.com/feed/update/urn:li:activity:6906533946969186304

If you can support our campaign on social media, in your email networks and newsletters, this would be hugely appreciated! Please do reach out if you would like to collaborate in any way!. Any support you can offer to our campaign is hugely welcomed and thank you for all you do – Pascale.robinson@praxis.org.uk

Share with our members something positive about your organisation’s achievement or service?

We were one of the organisations that helped to uncover the Windrush Scandal originally and we’re proud to have been part of the work to campaign to change the system.

What can other network members learn from you or find out more about through you?

- We can offer advice for those who need help navigating the migration system: Get Help — Praxis for Migrants and Refugees.

- We are experts in finding pathways out of destitution and supporting migrants facing homelessness. Please reach out to collaborate on this!

- We can offer training on the immigration system for a variety of organisations (depending on our capacity).

What would most help you achieve your goals?

We want to make sure that migrants can live in safety, overcome the barriers they face, and take control of their own destinies. To do this, we campaign for systemic change. We’re building alliances and working in partnership with experts by experience to create positive, long-term changes to the policies and practices that create exclusion and destitution. We’d love to collaborate on work to achieve these goals!

Why did you join 4in10? What do you enjoy about being part of the 4in10 network?

Though we have only been in contact with the 4in10 team for a short while, 4in10 has already provided a brilliant chance to forge connections and collaborate with other amazing organisations working in the capital!

We are so looking forward to working together more, especially on our campaign to make sure all who need them have access to free school meals regardless of their immigration status.

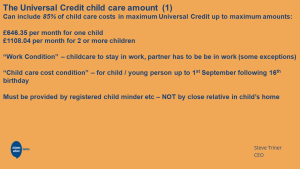

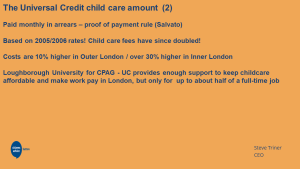

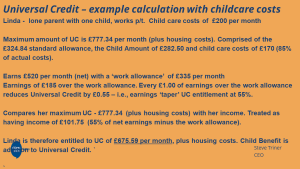

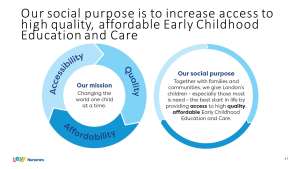

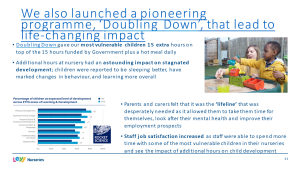

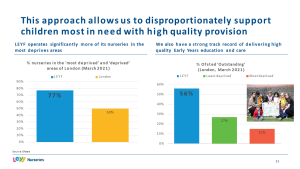

Fantastic 4in10 Coffee Morning on Child Care

4in10 Coffee Mornings are always full of great people and good things. Just to wet your appetite for future ones and to give you some insight into why we chose child care as the issue for today you can find the slides below.

Thanks to Steve Triner from Sutton CAB and Samantha Creme from the London Early Years Foundation.

4in10 Newsletter

The latest news, data, jobs, funding and more from 4in10, members and friends.

To get the latest issue directly to your inbox every other Thursday sign up here.

Proposals for a new Bill of Rights: what would it mean for children living in poverty in London?

Katherine Hill, 4in10’s Strategic Manager, takes us through the issues:

The story of Human Rights Act (HRA) reform has been a long and somewhat torturous one. Governments of various guises have been consulting on what changes might be needed since the mid-2000s, only a few years after the Act came into force. While the content of these proposals has changed over time the one constant has been that those who have made the effort to respond diligently to each round of consultation have almost unanimously concluded that there is no solid case for reform; the Act is doing the job it was intended to do, effectively defending ordinary citizens against the exercise of excess power or neglect by the state.

Most recently the Independent Human Rights Act Review (IHRAR) set up by the Government to take (yet) another look at the Human Rights Act reported that, “[t]he vast majority of submissions received by IHRAR spoke strongly in support of the HRA.” And the separate but concurrently running inquiry carried out by the cross-party Joint Committee on Human Rights concluded: “[t]o amend the Human Rights Act would be a huge risk to our constitutional settlement and to the enforcement of our rights”. Why, then, has the Government now published proposals for wide-ranging and significant changes to the way the Act works? We all know that evidence-based policy is out of fashion, but this seems to have gone one step further. It is embracing policy in that is in direct contradiction with the evidence. This is policy driven by ideology pure and simple.

At this, the temptation may be to throw up our hands and leave the beleaguered Human Rights Act to the hands of fate. What is the point of repeatedly making the case for it, only to be ignored? There are two reasons. Firstly, we must recognise that the case for effective human rights is one that needs to be constantly remade, it will never be a case of job done. Human rights, if they are to mean anything, must be a statement of collective values, an expression of our shared commitment to freedom, respect, equality, dignity and autonomy for all humans. For these to be transmitted from generation to generation there needs to be ongoing dialogue about them and what they mean in our modern world. Shying away from that conversation leaves the legal mechanisms we have for defending our rights vulnerable to attack.

Secondly, and more pragmatically, if we do not argue and win the case for the Human Rights Act, and these current proposals for reform come into force, ordinary citizens may lose the means to enforce their rights effectively. For those 4in10 exists to advocate with and for, families and children experiencing living in poverty in London, the consequences are potentially very serious indeed.

The proposed reforms aim in multiple ways to make it harder for people to enforce their rights. These include a proposal to introduce of a new step in the legal process requiring individuals to demonstrate that they had experienced “a significant disadvantage” before their case can go to court. Legal action can already only be taken if the individual is the “victim” of a human rights breach, so it is hard to view this as anything other than an attempt to deter people from enforcing their rights by adding a further legal hurdle to the process. This will disproportionately affect those experiencing poverty who are more likely to have their rights breached in the first place. To give just one example, children in the lowest income quintile are 4.5 times more likely to experience severe mental health problems than those in the highest.[1] It follows that some of those are more likely to experience mental health detention too, where their human rights – including the right to respect for private and family life (article 8) and right to liberty and security (article 5) – will be engaged. If children in these circumstances, who already find it very difficult to access justice, have to jump through additional hoops it will further diminish their ability to challenge their detention where they believe it is an unlawful breach of their human rights.

The Government’s proposals would introduce a two-tier system for enforcing human rights by restricting their use in the domestic courts by certain groups, including “foreign criminals” and those accused of illegal migration. This makes a mockery of the values underlying the whole notion of human rights. These are rights that everyone is entitled to enjoy regardless of economic or immigration status, gender, sexuality, disability or anything else. It follows that all should have equal access to the law to enforce them. If they don’t, the impact will be felt most by those on the margins, and especially the poorest children in our society. If the Government is more easily able to deport people without them being able to challenge this on the grounds of right to respect for private and family life (article 8), families may face the sudden loss of their main breadwinner, and children living in already financially precarious situations will be plunged into deeper poverty.

A key issue the Government seeks to address through its plans is that it wants to stop what is termed ‘judicial overreach’, that is the courts getting involved in decisions that are more properly the role of Government and Parliament, accountable as they are to the people. High on the list of things the Government believes it is best placed to make decisions about is the allocation of social and economic resources and it is particularly aggrieved when it thinks the courts seek to interfere in these issues.

The reality is however, that there is little evidence that this is what the courts in the UK are routinely doing. Recent cases that have examined welfare policy have often been unsuccessful, for example a challenge to the two-child limit (which does not allow welfare payments to be made to third and subsequent children) on the grounds that it discriminates against lone parents. The courts found these to be matters on which Parliament has deliberated and struck an appropriate balance. This may be very disappointing for those of us who believe that there should be a wider role for human rights in these matters, and that the right to an adequate income, a safe and warm home and access to healthy food meet basic human needs that should be enforceable whatever the colour of government in town. But it certainly does not support the Government’s argument for the need to curtail the powers of the courts, and the rights of individuals, as is proposed.

Over the longer-term we need to build the case and argue robustly for more comprehensive protection of these important economic, social and cultural in our domestic legal framework, as an essential element of any strategy to eradicate poverty. But first, and most urgently, we need to protect what we already have in the form of the Human Rights Act, as failing to do so will have the greatest impact on those who most need to rely on it.

To find out more about the Government’s plans to reform the Human Rights Act and to find out how you can respond to the consultation visit the British Institute of Human Rights dedicated web pages where you can find lots of easily digestible information and advice.

[1] Gutman, L., Joshi, H., Parsonage, M., & Schoon, I. (2015). Children of the new century: Mental health findings from the Millennium Cohort Study. London: Centre for Mental Health.

4in10 Newsletter 6th Jan 2022

Read our fortnightly newsletter here with news, calls to action, funding, jobs, free training and more. To receive this in your inbox every other Thursday just complete our . Everything is completely free!

4in10 Newsletter 09/12/21

4in10 Newsletter with data, reports, research, job vacancies, funding oopportunities and more. To read this issue click here. To receive the newsletter fortnightly straight to your inbox, join 4in10, London's child poverty network. It is completely free and gives advance notice of training and events and much more.

Timewise Video on Flexible Working

Timewise Webinar

Can flexible working help towards supporting low paid workers to progress and move out of poverty? Presenting the flexible working index and a discussion about flexible working as a real alternative.

https://timewise.co.uk/article/flexible-job-index-2021-a-timewise-roundtable/

Putting the onus on employers to enable all jobs to be flexible and for flexibility not to be a barrier to progression or keep people (mostly women) trapped in low paid work.

Fair By Design Blog. Innovation, fairness and a just transition to Net Zero

Fair By Design – The Poverty Premium.

Martin Coppack is Director at Fair By Design and Carl Packman is Head of Corporate Engagement and this article originally appeared on the Social Market Foundation website.”

By their very nature, essential services such as energy, credit, and insurance, are needed by everyone. However, these markets have been designed in a way that results in many people being treated less fairly. As Fair By Design’s research shows, poorer people pay more for products and services than those who are better off – known as the poverty premium.

The University of Bristol found that the poverty premium affects almost every low-income household, costing an extra £490 a year, on average. Low-income households experience the poverty premium in the energy market in a number of ways. They may use pre-payment meters for domestic fuel rather than paying by direct debit, or may prefer to pay on receipt of a bill to help manage a budget. Many low-income households are also not switched to the best fuel tariffs, which is also a poverty premium. These households are less likely to switch sometimes because they have other more pressing issues to deal with, which manifests in less capacity to engage in the market, which is known as the ‘scarcity mindset.’[1] It is not the same as consciously avoiding actions that might upset tight financial control, such as switching providers. They also may not be able to switch because of higher rates of digital exclusion, owing to a lack of ability or equipment to go online.

Research commissioned by Fair By Design found that people with certain protected characteristics are more likely to be paying a poverty premium, even when compared with low-income households as a whole. People from Black, Asian, and other ethnic minority households are more likely to be paying extra costs for energy, and paying on receipt of a bill, rather than by direct debit, which is usually cheaper. Single parents are more likely to pay for energy through more expensive prepayment meters. These groups are more likely to be in low-paid or insecure work and therefore need flexible payment methods to help keep control of their finances. Disabled people are more likely to be paying by either of these methods, than non-disabled people.

The poverty premium is particularly pertinent at the moment since poorer households suffer disproportionately in hard times. There are now millions more people facing economic hardship as a result of the pandemic. The ongoing gas price crisis means that the cost of heating the average home could also double.

Why does the poverty premium exist?

Essential products and services are too often designed for ‘super consumers.’ These are people who never become ill, always have a steady income, are able to understand complex terms and conditions and always have the time and technology to easily find the best deal. This is not a reality for everyone. There is a disconnect between social and regulatory policymakers and people’s lived experiences of poverty and exclusion, and a belief that a market based on competition benefits all consumers. In practice, firms compete for the most profitable and engaged consumers. It means that for many people products and services do not meet their needs or even that they are excluded altogether.

Inclusive Design: Understanding how different groups and consumers experience products

Across essential services regulators, inclusive design is increasingly recognised as a way to ensure markets are fair and inclusive, especially for consumers in vulnerable circumstances and on low incomes.

Inclusive design is a toolbox that helps design products and services that are accessible to as many people as possible. It is different to ‘traditional’ market research in that it is not simply about testing pre-existing solutions and hypotheses. It starts by talking to people with additional needs to understand the problems from their perspective, and designing from there. Rather than shaping the consumer around the product or service, firms start with people where they are, and co-design with them. This is especially important as the energy system becomes increasingly digitised, and we transition to net zero.

Instead of designing for a mythical ‘average’ user, firms should therefore understand people’s actual experiences and how these might put them at a disadvantage. In other words, what are they vulnerable to, and why?

There are huge benefits to firms from adopting an inclusive design approach. By involving customers in the process of product design and development, it increases the likelihood of adoption, and reduces the need for solving problems after they occur, through customer service, for example.

The role of government and regulators

At the same time we know that firms will only design inclusively, to a point. There are always going to be some consumers that are deemed less desirable and for whom competition alone will not help. Markets need to be regulated to serve everybody. This means that Government (BEIS) and regulators (Ofgem) should not only be encouraging firms to design inclusively, they should be applying inclusive design principles to their own work. They should shape their own policies around the consumer, especially those most vulnerable and least heard – rather than trying to make such consumers fit their desired regulatory intervention. It is not enough to rely on competition and the belief that empowered consumers drive the market.

For instance, consumers have a role in designing the appropriate policy steps towards decarbonisation. This is very important, since we need to ensure that the cost of the transition to renewable energy sources is not placed disproportionately and unfairly on low income groups. Although many UK households are reportedly willing to accept some increase in their bills to help finance the future energy transition, this will not be possible for all households – particularly those with little slack in their existing household budgets, or who do not own their own home.

Ofgem and BEIS should adopt an inclusive design approach to understanding the needs of all consumers (particularly those on low incomes) and use this approach to help set their priorities, develop and implement interventions, and assess their effectiveness. This means doing things differently, and engaging with low income people directly – placing them at the heart of decisions.

To help with this, Fair By Design, along with our partners Money Advice Trust, has published a practical guide on what inclusive design means and how it can be incorporated into the work of regulators.

The future of price protections

An inclusive design approach to policymaking will help identify where the limits are for the market serving certain groups of consumers, and for whom additional protections – such as price caps and targeted “social” tariffs – are needed.

In a Fair By Design study of low income households accessing Turn2us’ services, researchers compared the costs of the energy poverty premium in 2016 and 2019 to assess the degree to which the retail energy market has changed. [2] While their findings showed the positive impact of regulation, low-income consumers still face excess costs for their energy.

For example, the gap between the Standard Variable Tariff and the best online-only fixed tariff had reduced from £317 in 2016, to £213 in 2019, a reduction of over £100. [3] The gap between the best pre-payment meter tariff and the best online-only fixed tariff had almost halved, dropping from £227 in 2016 to £131 in 2019.[4] This shows a strong correlation between price protections and a reduction in the poverty premium.

This is very welcome news and shows that sensible regulation and a focus on price to protect consumers is achieving good outcomes. The focus now should be on how to narrow the gap even further, to entirely remove the poverty premium, through a combination of inclusively-designed innovations and policy changes.

About Fair By Design

Fair By Design is dedicated to reshaping essential services, such as energy, credit and insurance, so they don’t cost more if you’re poor. People on low incomes and in poverty pay more for a range of products including energy, through standard variable tariffs; loans and credit cards, because of higher interest rates; and expensive insurance premiums, by living in postcodes considered higher risk. This is known as the poverty premium.

We collaborate with industry, government, and regulators to design out the poverty premium. Our Venture Fund provides capital to help grow new and scalable ventures that are innovating to make markets fairer. The Barrow Cadbury Trust runs our advocacy work, and Ascension manages the Venture Fund.

To download the Fair By Design and the money Advice Trust guides on inclusive design visit: https://fairbydesign.com/inclusive-design/ There is one for regulators (and social policy makers) as well as one for firms.

Notes

- [1] Scarcity: The True Cost of Not Having Enough, Sendhil Mullainathan & Eldar Shafir (2011)

- [2] Although average figures of the poverty premium are not comparable across the two studies, due to differences in methodology, the calculation of the premiums remained the same and so costs are comparable.

- [3] Drawn from the average across Big 6 suppliers and across household size.

- [4] Drawn from the average across Big 6 suppliers and across household size.

Camden Federation of Tenants Briefing for VCS's

Background

There is a greater focus on the private rented sector (PRS) than ever before, but because of the media’s excessive interest in so-called “Generation Rent” there is a misconception that most people who live in it are mostly students and highly paid young professionals.

While a significant number of both of these groups rent privately across London, it would be wrong to assume that all of them are well off. Increasingly, the PRS is now made up of a mixture of household types and recent research carried out by the University of York* identified these six as being the most “vulnerable to harm” in the PRS.

1. With dependent children

2. With someone registered as disabled or who is unable to work due to a long-term sickness or

disability

3. With someone aged 65 or older

4. In receipt of a means tested benefit or tax credit

5. On a low-income but not receiving any means tested benefits or tax credits

6. Headed by a recent overseas migrant